In theory, Bitcoin mining stocks seem like a convenient way to gain Bitcoin exposure, after all, these companies’ core business is producing BTC. But recent data reveals a harsh reality: many public miners are producing Bitcoin at a higher cost than Bitcoin’s market value. In Q4 2024, several publicly traded Bitcoin mining companies had all-in costs per coin well above the average Bitcoin price of ~$83,000†. In other words, they were mining at a loss. Meanwhile, MiningStore’s own mining program was producing Bitcoin for a fraction of that cost.

Source:

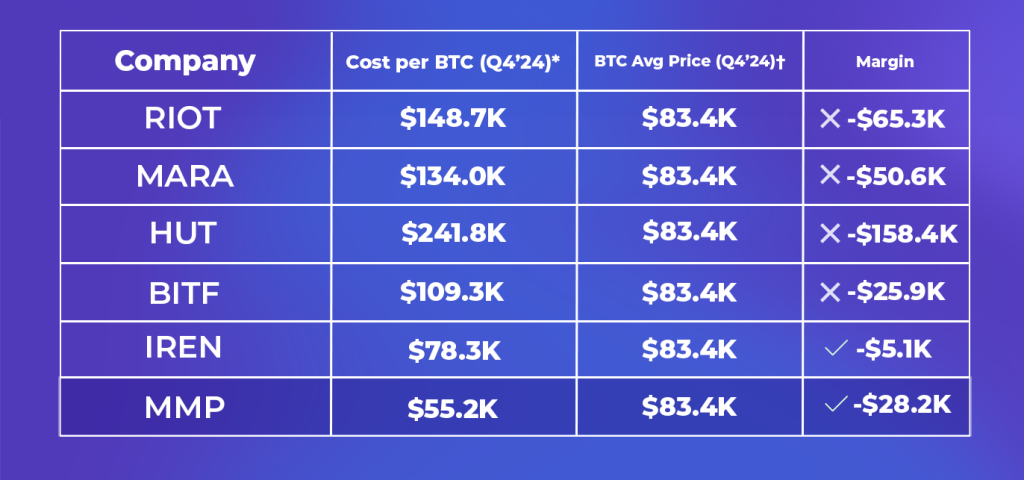

* Data from @matthew_sigel on Twitter. Retrieved from https://x.com/matthew_sigel/status/1908123263525327163

† StatMuse, Average Bitcoin price in Q4 2024 $83,426. Retrieved from https://www.statmuse.com/money/ask/bitcoin-average-price-q4-2024

‡ MMP cost per BTC is based on Antminer S21 Pro. Actual costs may vary by machine type and deployment conditions.

As shown above, most public miners in late 2024 were underwater on each coin mined, spending more to mine 1 BTC than the market value of that BTC. Riot spent about $148k per coin and Marathon $134k, while Bitcoin averaged ~$83k. By contrast, MiningStore’s MMP participants mined Bitcoin at roughly $55k all-in, leaving a healthy ~$28k gross profit per BTC. Even the more efficient public miner (Iris Energy) only eked out ~$5k profit per coin, and others lost tens of thousands of dollars per coin. This huge cost disparity translates to vastly different mining margins, and ultimately ROI for investors.

Why are the costs for public miners so high? Simply put, publicly traded Bitcoin miners operate like large enterprises, and they carry all the baggage that comes with it:

- Bloated overhead: massive SG&A expenses, corporate offices, and layers of management.

- High executive compensation: multi-million dollar CEO and board pay.

- Bureaucracy and compliance: costs for legal teams, HR, regulatory compliance and reporting.

- Investor pressures: they often prioritize quarterly stock performance over efficiency, leading to suboptimal decisions and dilution of equity.

They don’t just mine Bitcoin; they manage boardrooms and internal politics. As an investor buying their stock, you’re footing the bill for all that overhead. You get whatever’s left after executives, lawyers, and accountants are paid, which lately, as the data shows, has been nothing but red ink.

On top of slim (or negative) margins, mining stocks add extreme volatility. These stocks act like high-beta Bitcoin proxies, often swinging more wildly than Bitcoin’s price itself. For example, during the 2022 crypto bear market, Bitcoin fell about 65%, but Marathon’s stock plunged around 80–90% from its highs. Riot’s share price has been about 60% more volatile than Bitcoin’s, and Marathon’s about 40% more. In plain terms, a 10% drop in BTC might trigger a 20%+ drop in those miner stocks. Investors in mining equities take on greater downside risk without any guaranteed Bitcoin yield, a double whammy of risk and inefficiency.

And crucially, unlike traditional dividend-paying companies, most public miners do not share the Bitcoin they mine with shareholders. They typically reinvest or hold it on their balance sheet. That means as a stock investor, you receive no direct BTC yield or dividend from the mining operations. Your only hope of profit is the stock price going up, which depends on market hype and those very same inefficient operations improving.